ShekouDaily | May 10, 2017

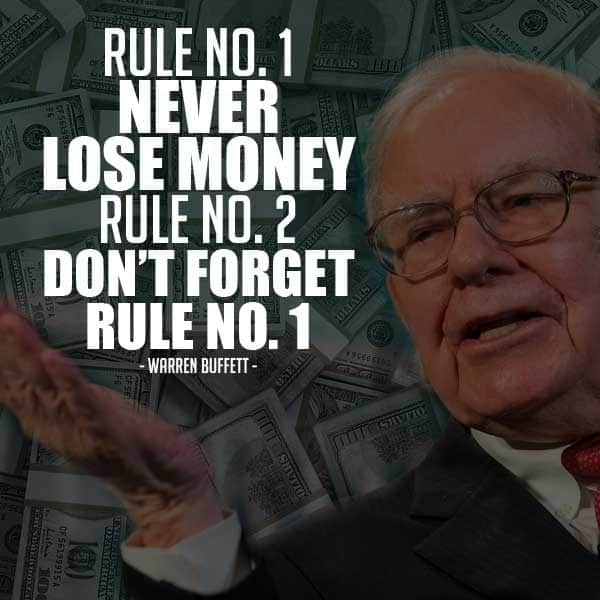

Warren Buffet, perhaps the greatest investor of all time, stated one of my favorite quotes that we should all try to live by.

“The first rule of investing is don’t lose money; the second rule is don’t forget Rule No. 1.”

Buffet is quite the frugal guy. He’s known for eating McDonald’s breakfasts that cost less than $5 every morning, living in the same house he purchased back in the 80’s in Nebraska, and driving a Cadillac. It’s definitely not comparable to some of the other richest billionaires on the planet, but that’s what makes Mr. Buffet so unique.

As a financial advisor, one of the biggest problems I see is debt. Debt can certainly destroy your finances, so here are a few tips to keep in mind not only for yourself, but also for your children. Studies show financial savviness can be learned from a young age.

Beware of Credit Cards

Credit card debt is a serious problem. Every time you use your credit card, you are taking out a small loan with an interest rate. This not only means you’re putting yourself in debt every time you use your beloved credit card, but also that the debt is growing. Here’s an example.

Let’s say you went on a shopping spree at Apple. All the cool gadgets costed $10,000, and you used your credit card to pay the bill.

However, let’s say you don’t have $10,000 to pay the credit card company back. If the credit card company had an interest rate of 5% (which is quite low for credit card companies), after 15 years you would owe that company $20,789!

If the interest rate was 18% (which is more in line with many credit card companies out there), at the end of 15 years you would owe them a whopping $119,737!!!

Credit card debt isn’t something to be taken lightly…

Other Debt Traps

Credit cards aren’t the only debt traps out there. There are many. Mortgages, bank loans, and even student loans (you definitely want to talk to your kids about this, read this article on education planning for more) can all cause serious damage to your finances. Before you borrow money, make sure to follow these useful tips.

Tips for Combating Debt

The best rule for combating debt is to stay debt free, but that can often be impossible in today’s world. Luckily, there are a few tips to help you navigate through the choppy seas of debt.

1. Don’t spend what you can’t afford. If you don’t have $10,000 to go on a shopping spree at Apple, don’t spend it!

2. Always read the fine print when taking out a loan. If the interest rate is really low, then it could be a safe loan. If it’s very high, you may want to think again.

3. Assess your circumstances — weigh in on risk vs. rewards. If you get accepted to Harvard and need a loan, that could very well be a great investment that would allow you to pay off that loan quickly. In this case, getting a student loan could be a great idea.

As you can see, debt can not only hamper your credit score, but also you and your family’s financial health. Let’s all be good investors, and always try to follow Warren Buffet’s motto of never forgetting Rule No. 1!

About the Author: Dewey (Trey) Archer

Dewey (Trey) Archer has been a Financial Consultant with Infinity Financial Solution, Ltd since 2014. He is qualified by the Chartered Insurance Institute (CII) with an Award in Financial Planning and has been awarded the title of Premier Advisor at Investopedia Advisor Insights. His studies and career have taken him to over one hundred countries, and his international experience has allowed him to add Spanish, Portuguese and Mandarin (along with his native English) to his list of fluent languages. Trey specializes in IRS compliant investments and pensions for American nationals but enjoys using his international background and linguistic skills to work with a vast network of people from all over the globe. Trey can be reached at +86 138 1620 7274 or [email protected]