Now Shenzhen | January 31, 2023

Item 1 of Ministry of Finance and State Taxation Administration Announcement [2019] No. 35)” (hereinafter referred to as “Announcement No. 35”) in 2019 stipulates that when an individual without domicile makes his first declaration in a tax year, he or she shall calculate and pay the tax according to the estimated number of days of residence in a tax year and the number of days of stay in China within the period specified in the tax treaty according to the contract.

In the previous article, we shared the individual income tax treatment after residents turns to non-residents:

IIT Treatment from Residents to Non-Residents

Today, we will share how to deal with the individual income tax after a non-resident individual turns to a resident individual after he/she reaches the condition of resident individual due to the extension of residence days in a tax year.

DEFINITION

Resident Individuals

Resident individuals for IIT purposes include the following two categories:

① Chinese citizens and foreign nationals who have a domicile in China. This does not include Chinese citizens who reside in Hong Kong SAR, Macau SAR, Taiwan region, or overseas but who do not have a domicile in the Chinese Mainland.

② Foreign individuals, overseas Chinese and residents of Hong Kong SAR, Macau SAR and Taiwan region who do not have a domicile in China’s Mainland but who have stayed in China’s Mainland for a total of 183 days or longer in a single tax year.

Non-resident Individuals

Non-resident individuals refer to an individual who meet one of the following conditions: individuals who have no domicile and do not reside in China’s Mainland; or individuals who have no domicile in China’s Mainland and who have stayed in China’s Mainland for less than 183 days in total in a single tax year.

Domicile

Having a domicile refers to maintaining a habitual residence in China for the purposes of permanent residence, family or economic interests, rather than merely owning real estate in China. If an individual resides outside China only for study, work, family visits, travel, etc., and then must return to live in China after the aforesaid activities are completed, the individual’s habitual residence shall be deemed to be in China. Conversely, if an individual resides in China only for study, work, family visits, travel, etc., and then leaves to reside abroad once the aforesaid activities are completed, the individual’s habitual residence shall be deemed to not be in China (such individuals are hereinafter referred to as “nondomiciled individuals”). For example, if a foreign individual purchases real estate in Shenzhen as an investment, the individual will not be deemed to have a domicile in China based merely on his or her ownership of the real estate.

It should be noted that the concept of “in China” in prevailing Chinese tax laws refers only to China’s Mainland and does not include Hong Kong SAR, Macau SAR and Taiwan region. In the following sections, we will use “in China” and “outside China” to differentiate.

Law and Regulations

According to the provisions of Announcement No. 35, where a non-domiciled individual is predetermined to be a non-resident individual but ultimately satisfies the resident individual criteria due to the extended number of days he or she stays in China, the tax withholding method within the tax year shall remain unchanged, and the individual shall complete the reconciliation filing and payment procedures at the end of the year pursuant to the relevant provisions for resident individuals. However, if the individual leaves China during the year and is not expected to enter China again during the estimated year, he or she may opt to complete the reconciliation filing and payment procedures before leaving China.

EXAMPLE

A is a U.S. citizen who is employed by company B in China at the beginning of 2021 and plans to come to China to work, and the expected work period is from February 1, 2021 to June 30, 2021.

So how should company B withhold and pay the individual income tax for A?

First of all, company B should first estimate A’s residence time in 2021 according to the number of days of residence in the country within a tax year as estimated in the contract and the number of days of stay in the country within the period stipulated in the tax treaty when making the first individual income tax withholding and payment declaration for A in the current year.

According to the contract, A qualifies as a non-resident tax payer, and company B calculates and withholds and pays individual income tax for A as a non-resident individual. However, the actual situation is different from the estimated situation, A extends the labor contract to December 31, 2021 for work reason, resulting in A’s actual residence in China for more than 183 days to meet the resident individual condition, how should his individual income tax be handled?

According to the provisions of Announcement No. 35, it should be reported to the competent tax authorities between March 1, 2022 and June 30, 2022 for the conversion of non-resident to resident and recalculate A’s taxable amount according to the resident individual.

Assuming A is a non-executive, has no foreign income during his employment with company B, salary is 30,000CNY per month, rent special additional deductions is 1500CNY per month, and pays a personal social insurance of 3,000CNY per month, regardless of mutual tax treaties. How much difference is individual income tax from the a non-resident to a resident?

Non-resident Tax Calculation

For the period from February 2021 to December 2021, A’s individual income tax is calculated as follows:

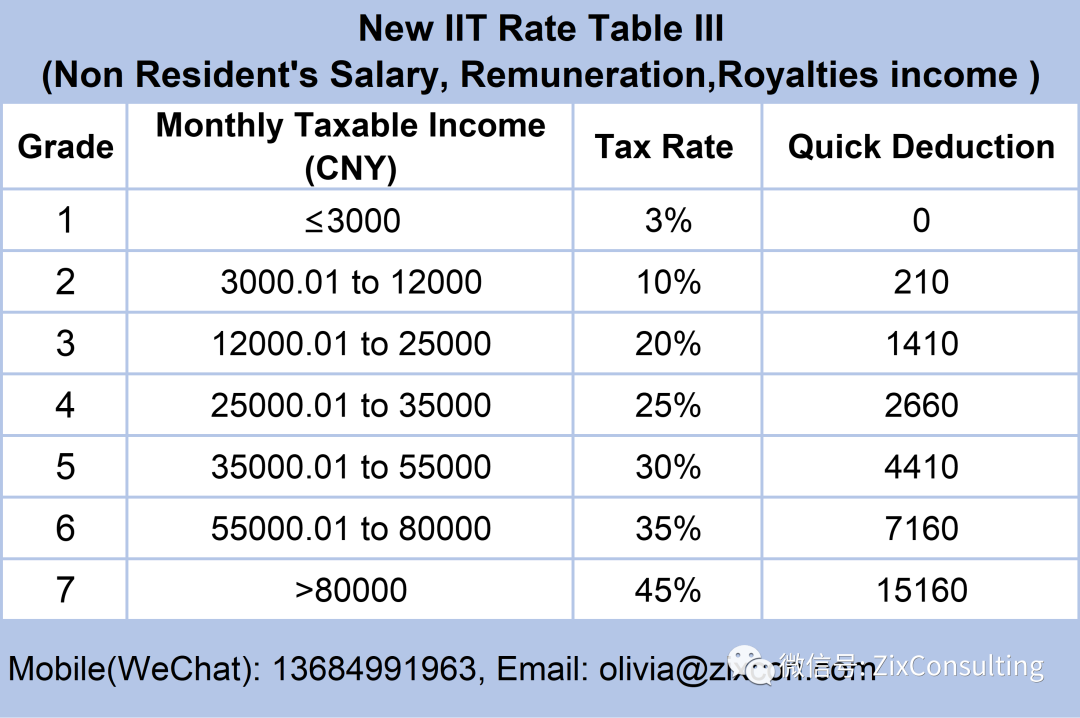

According to Tax Rate Table III, monthly taxable income: 30,000-3,000-5,000=22,000, the corresponding tax rate is 20% and the quick deduction is 1410.

Monthly tax amount: 22000*20%-1410=2990.

Total tax from Feb to Dec: 2990*11=32890CNY.

Non-Resident IIT Table III:

Resident Tax Calculation

However, he needs to recalculate his individual income tax as a resident individual because A’s actual period of residence qualifies as a resident individual. Salaries earned by a resident individual should be calculated as annual comprehensive income for individual income tax purposes.

Taxable income as a resident individual:

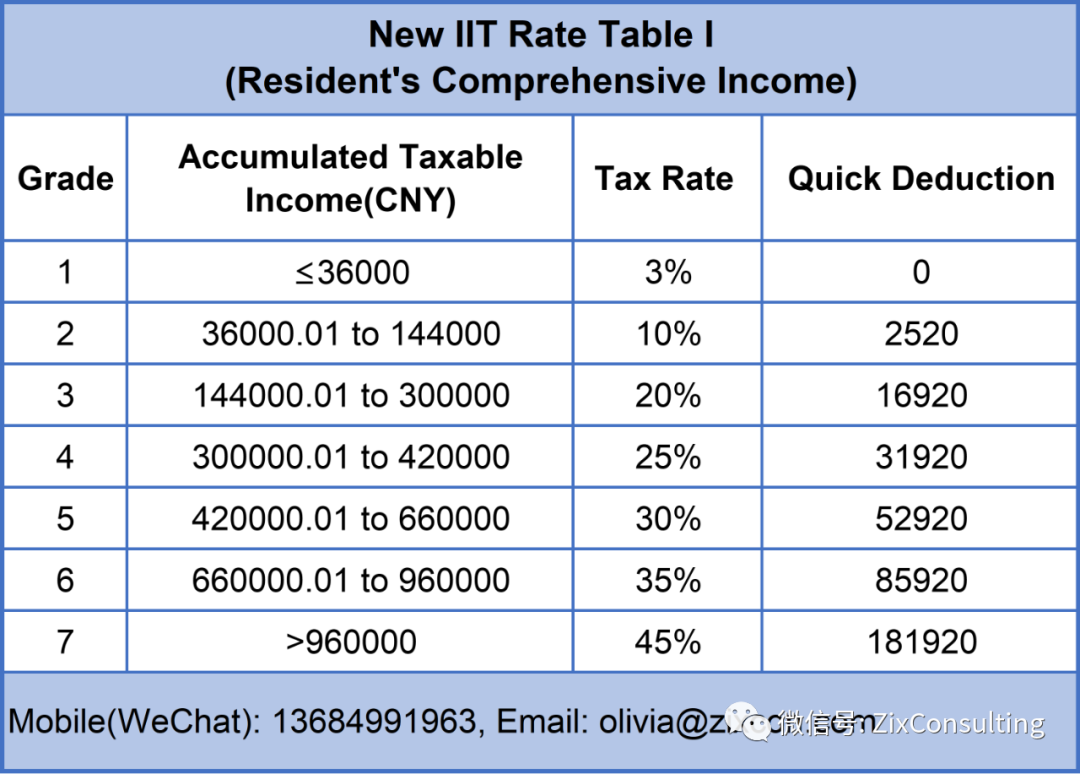

According to IIT Rate Table I, annual taxable income: 30000*11-3000*11-1500*11-5000*12=217,500CNY, corresponding tax rate is 20%, quick deduction is 16920.

The tax amount from Feb to Dec is: 217500*20%-16920=26,580CNY.

Resident IIT rate table I:

Tax Refund

The amount of IIT payable for the year based on resident individual is: 26,580CNY.

The actual amount paid: 32,890CNY.

A can get tax refund: 32890-26580=6310CNY.

IIT Settlement

1.Content of Settlement

According to the IIT law, a tax resident individual, is required, after the year-end, to report the total amount of four types of income including salary and wages, remuneration for independent services, income from author’s remuneration, and royalties (hereinafter referred to as “comprehensive income”) derived in a tax year from January 1 to December 31. In this case, the standard deduction of RMB60, 000, itemized deductions, additional itemized deductions, other eligible deductions, and qualifying charitable donations would be deducted from the total income received to arrive at the taxable income, which would then be multiplied by the applicable tax rate on comprehensive income and subtracting the corresponding quick deduction to arrive at the final tax liability for the year. The tax due or refundable is the tax liability minus the tax prepayment. Taxpayers shall perform a tax filing with the tax authorities to settle the tax payable or apply for a refund.

The IIT calculation for comprehensive income is below:

IIT payable (or refundable) on comprehensive income for the year = [Total annual comprehensive income – standard deduction of RMB 60,000 – itemized deductions (i.e., social insurance and housing funds) – additional itemized deductions (i.e., education) – other eligible deductions – charitable donations) × applicable tax rate – quick deduction] – IIT pre- paid for the year.

2. Filing Methods

There are three main ways to perform annual IIT reconciliation filing: self-declaration, authorizing employer or authorizing a third party to handle on behalf of the taxpayers.

Firstly, self-declaration. That is, the taxpayer files the returns by himself/herself. The taxpayer can perform annual IIT reconciliation filing via the IIT APP in mobile phones or e-Tax Bureau for individual taxpayers from PC end.

Secondly, to authorize the Employer to file the returns. The taxpayer can choose to authorize his/her employer to file the returns, or consult with the employer for guidance on how to file annual returns via the IIT APP in mobile phones or e-Tax Bureau for individual taxpayers from PC end. Taxpayers who choose to authorize the Employer to file the returns shall confirm the authorization with the company via written or electronic method(s) by April 30 of the following year. In the meantime, if the taxpayer has other personal income not derived from the authorized employer, or other deductions that the authorized employer does not have the related information, the taxpayer needs to provide the full information to the employer, and shall be self-responsible on the authenticity, accuracy and integrity of the information provided.

Thirdly, to authorize a third party (i.e., tax related professional service agent/ other organization/person) to file the returns. Under this method, a written Letter of Attorney is advised to be arranged to clear the rights, responsibilities and obligations of the authorized party and the taxpayer.

3. Circumstances Not

Required Settlement

Taxpayers who have paid individual income tax in advance in accordance with the law during the tax year and meet one of the following circumstances are not required to apply for annual settlement:

(1) The annual settlement is subject to tax reimbursement but the annual comprehensive income does not exceed 120,000 CNY;

(2) The amount of tax remittance required for the annual remittance does not exceed 400CNY;

(3) The amount of tax already prepaid is consistent with the amount of tax payable in the annual remittance.

(4) Those who meet the conditions of annual tax remittance but do not apply for tax refund.

4. Conditions Required

Settlement

Taxpayers are required to apply for annual settlement if one of the following circumstances is met:

(1) The prepaid tax amount is more than the taxable amount in the annual settlement and applies for tax refund.

(2) The comprehensive income obtained in the tax year exceeds 120,000 CNY and the amount of tax reimbursement exceeds 400CNY.

(3) There are special additional deductions eligible for entitlement, but no deduction is declared when the tax is prepaid.

(4) Deductions of 60,000CNY, special deductions such as “three insurance and one fund”, special additional deductions such as children’s education, corporate (occupational) annuities and deductions such as commercial health insurance and tax-deferred pension insurance are not sufficient due to mid-year employment, retirement or lack of income in some months, etc.

(5) Those who do not have an employer and only receive remuneration for services, remuneration for writing, royalties, and need to make various pre-tax deductions through annual settlement.

(6) Taxpayers whose prepaid tax amount is less than the taxable amount and should pay the tax due, such as:

A. Taxpayer changed the employment in different companies during the year, and after the combination of annual comprehensive income, the applicable annual tax rate is higher than the tax rate adopted in the prepayment.

B. Other than income from salary and wages, the taxpayer also receive remuneration for independent services, author’s remuneration and income from loyalties. After the combination of all the annual comprehensive income, the applicable annual tax rate is higher than the tax rate adopted in the prepayment.

If a taxpayer under-declares or fails to declare the comprehensive income during the tax year due to the error of the applicable income items or the withholding agent’s failure to fulfill the withholding obligation according to law, the taxpayer shall proceed with the annual settlement according to the law.

We can provide individual income tax accounting, individual income tax annual settlement, individual income tax consultation, individual income tax subsidy application for foreign high-end talents, company tax planning, company bookkeeping and tax reporting, etc.!